Managing money isn’t particularly complicated in theory. Most people understand the basics: spend less than you earn, save consistently, avoid unnecessary debt, and plan for the future. The challenge is that knowing what to do and doing it consistently are often two very different things.

Table of Contents

- 1. Build Systems Before Setting Bigger Financial Goals

- 2. Save First, Not Last

- 3. Review Your Finances Monthly Instead of Daily

- 4. Create Rules for Impulse Purchases

- 5. Plan for Expenses You Know Are Coming

- 6. Improve One Money Habit at a Time

- 7. Focus on Consistency Before Optimization

- Consistency Beats Complexity

This is one reason personal money management tips can feel frustrating. Much of the advice available today is technically correct, yet many people still struggle to improve their financial situation. The issue is rarely a complete lack of information. Instead, it’s the difficulty of turning good advice into habits that can be maintained over months and years.

A budget can be created in an afternoon. A savings goal can be written down in a few minutes. A financial app can be downloaded in seconds. None of those actions guarantee long-term progress. What ultimately matters is consistency.

The most effective money management tips are rarely the most sophisticated. They’re usually the ones that fit naturally into everyday life and become part of your routine. Over time, those routines shape financial decisions, influence spending behaviour, and create the foundation for lasting financial stability.

In this guide, we’ll look at seven money management tips that are practical, sustainable, and realistic enough to maintain long after the initial motivation wears off.

1. Build Systems Before Setting Bigger Financial Goals

Financial goals are important because they give your money direction and help you identify what you’re working toward. Whether you’re trying to build an emergency fund, pay off debt, save for a home, or achieve greater financial independence, goals provide a destination. What goals don’t provide is a reliable way to get there.

This is where many people run into trouble. A common assumption in personal finance is that success starts with setting better goals. While goals certainly matter, they are only one part of the equation. A goal without a supporting system is often little more than a good intention.

Imagine two people who both want to save $5,000 over the next year. The first person writes the goal down, feels motivated, and promises to save more money each month. The second person sets up an automatic transfer that moves money into a savings account every payday.

Both people have the same goal, but only one has built a system designed to support it.

Several months later, it’s easy to predict which person is more likely to make meaningful progress.

This principle extends far beyond saving money. People often focus on outcomes while overlooking the behaviours that create those outcomes. They want to pay off debt, spend less, invest more, or improve their money habits, yet the systems required to support those goals are rarely given the same level of attention.

A stronger approach is to build the process first and allow the results to follow. Instead of asking, “How much do I want to save this year?” it can be more useful to ask, “What system will help me save consistently?” Instead of asking, “How can I stop overspending?” consider asking, “What changes can I make that reduce the temptation to overspend in the first place?”

The answers to those questions tend to produce better long-term results because they focus on actions rather than intentions.

One of the most useful personal money management tips is to stop treating goals as the starting point. Goals tell you where you want to go. Systems determine whether you get there.

2. Save First, Not Last

One of the oldest pieces of financial advice is to save whatever remains at the end of the month. While this approach sounds sensible, it often fails in practice because life has a habit of filling the space between payday and month-end.

Bills arrive. Unexpected expenses appear. Social events come up. Small purchases accumulate. Before long, there isn’t much left to save.

This is why one of the most effective money management tips is to reverse the process and save first instead of last.

When savings become the first financial priority rather than the final consideration, they are far more likely to happen consistently. Many people find success by automatically transferring a portion of their income into a separate savings account shortly after getting paid. The amount itself matters less than the consistency of the habit.

This idea may seem simple, but it reflects a larger principle within personal finance. Financial progress often depends less on making perfect decisions and more on removing opportunities to make poor ones.

When saving depends entirely on self-control, it becomes vulnerable to competing priorities. When saving is automated or scheduled in advance, the decision has already been made.

A common misconception is that saving money only becomes possible once income reaches a certain level. While a higher income certainly creates more flexibility, the habit of saving and the amount being saved are two different things. Someone who consistently saves a small percentage of their income is often building a stronger financial foundation than someone who intends to save later but never develops the habit.

This doesn’t mean everyone should save the same amount. Personal finance is rarely that simple. Income levels, living costs, family responsibilities, and financial goals vary from person to person. What matters is creating a system that allows saving to happen regularly without requiring constant effort or motivation.

Over time, small amounts accumulate. More importantly, the habit becomes part of your financial routine. That’s where the real value lies. A healthy financial system isn’t built around occasional bursts of discipline. It’s built around behaviours that can be repeated consistently for years.

3. Review Your Finances Monthly Instead of Daily

Financial awareness is important, but there is a difference between being informed and becoming consumed by every financial decision.

Many people assume that managing money effectively requires constant monitoring. They check bank balances daily, review investment accounts several times a week, and track every financial movement as though they are monitoring a stock market portfolio.

For a small group of people, this level of attention may be useful. For most people, it creates unnecessary stress without significantly improving financial outcomes.

One of the more overlooked personal money management tips is to establish a regular review process rather than turning money into a daily obsession.

A monthly financial review allows you to step back and assess the bigger picture. You can evaluate spending patterns, monitor progress toward savings goals, review upcoming expenses, and identify areas that need attention without feeling pressured to react to every minor fluctuation.

This approach is particularly helpful because financial progress rarely happens on a daily basis. Most meaningful changes become visible over weeks and months rather than hours and days.

Consider someone trying to improve their spending habits. Looking at their account balance every morning may increase awareness, but it doesn’t necessarily provide useful insights. Reviewing a month’s worth of spending, on the other hand, reveals patterns. It becomes easier to identify recurring expenses, recognise unnecessary spending, and make informed adjustments.

The same principle applies to savings goals and debt repayment. A single day rarely tells you much. A month often tells a story.

This is where many financial habits break down. People start with intense enthusiasm, monitor everything closely for a few weeks, become overwhelmed, and eventually abandon the process altogether. A monthly review is more sustainable because it provides structure without creating constant pressure.

One way to approach this is to schedule a recurring “money date” with yourself at the end of each month. Spend thirty minutes reviewing your income, expenses, savings, debts, and financial goals. Celebrate areas where you’ve made progress and identify areas that need attention.

The purpose isn’t to judge yourself. It’s to stay informed.

Managing money should help reduce financial stress, not create more of it. A monthly review often provides enough visibility to make better decisions while allowing you to focus the rest of your time and energy on living your life.

4. Create Rules for Impulse Purchases

Impulse purchases are often treated as a discipline problem. The usual advice is straightforward: stop buying things you don’t need. While that sounds reasonable, it doesn’t explain why so many people continue making purchases they later regret.

The reality is that impulse spending rarely happens because someone consciously decides to make a poor financial choice. It usually happens because a decision is made in the moment, influenced by convenience, emotion, excitement, or the fear of missing out.

This is why creating rules around spending is often more effective than relying on willpower alone.

One simple example is the 24-hour rule. Before making a non-essential purchase, wait 24 hours before completing the transaction. For larger purchases, some people extend this waiting period to 48 hours or even a week.

The purpose isn’t to prevent spending. It’s to create enough space between the desire to buy something and the decision to spend money on it.

Many purchases that feel urgent in the moment lose their appeal after a short period of reflection. Others may still feel worthwhile, but the delay provides an opportunity to consider whether the purchase aligns with your priorities and financial goals.

This approach reflects a broader principle within money management tips. Good financial decisions are often easier when they are made deliberately rather than emotionally.

Not every impulse purchase is harmful, and nobody needs to justify every dollar they spend. The objective is simply to reduce the number of decisions you later wish you had approached differently.

Over time, these small spending rules can strengthen your money habits without making you feel restricted. Instead of constantly asking yourself whether you have enough discipline, you create a framework that helps better decisions happen naturally.

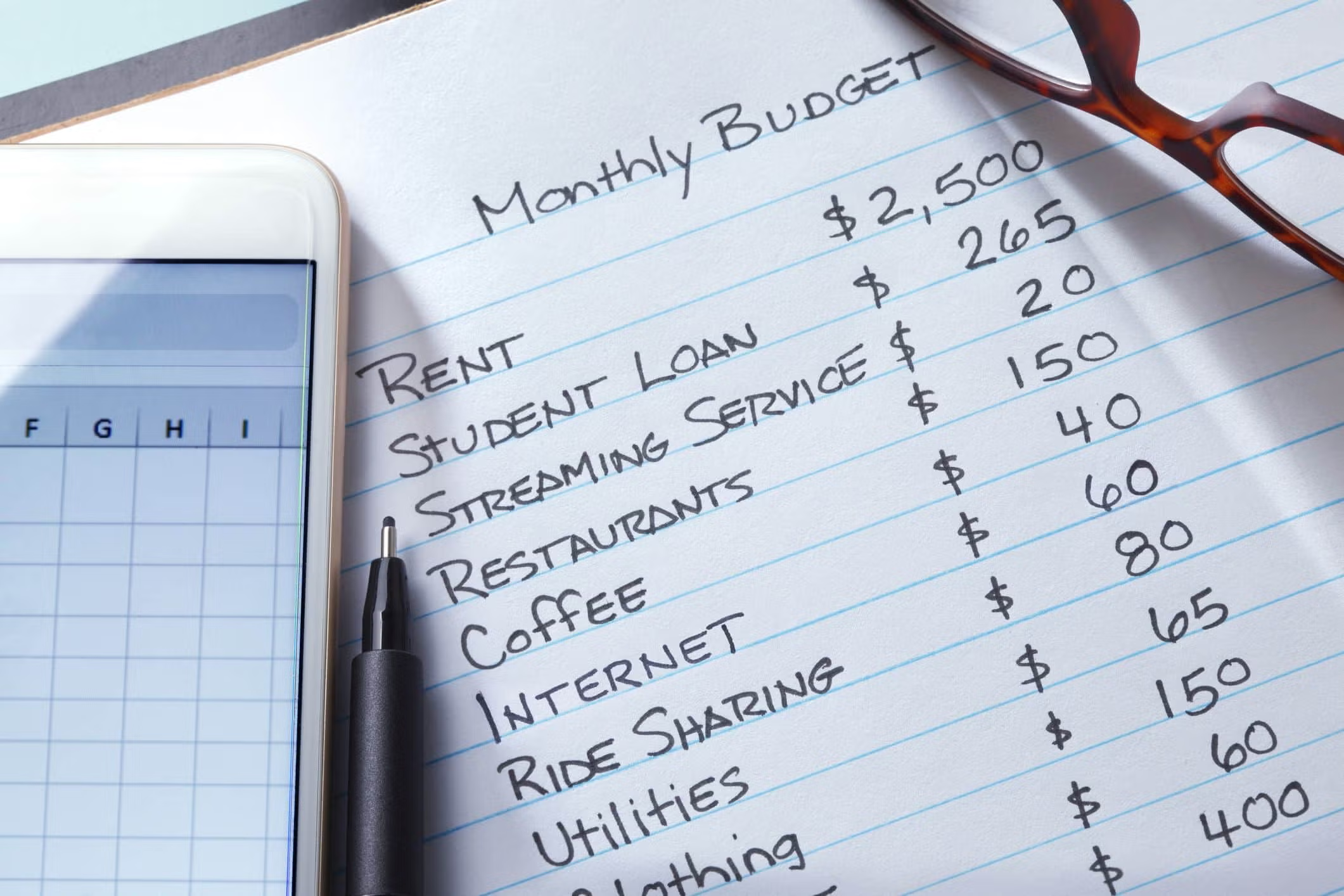

5. Plan for Expenses You Know Are Coming

One reason financial plans fail is that they are often built around monthly expenses while ignoring costs that occur less frequently.

Rent, utilities, subscriptions, and loan payments are easy to remember because they appear regularly. The challenge comes from expenses that arrive once or twice a year but are entirely predictable.

Birthdays happen every year. Holidays happen every year. Insurance renewals, annual memberships, school expenses, vehicle maintenance, and home repairs are all part of normal life. Yet many people continue treating these costs as unexpected.

When these expenses arrive, they can disrupt a budget, reduce savings progress, or force people to rely on debt. This creates the impression that the financial plan isn’t working when the real issue is that the plan wasn’t designed to account for reality.

One of the most valuable money management tips for beginners is to start thinking beyond the current month.

A practical way to do this is to identify recurring annual expenses and divide them by twelve. If you know you’ll spend $600 on holiday gifts later in the year, setting aside $50 per month can make that expense far easier to manage. The same principle applies to insurance premiums, maintenance costs, and other predictable obligations.

This may not feel as exciting as investing or paying off debt, but it often has a greater impact on day-to-day financial stability.

Many financial setbacks aren’t caused by major emergencies. They’re caused by predictable expenses that were never included in the plan.

Planning ahead doesn’t eliminate those expenses, but it does remove much of the stress associated with them.

6. Improve One Money Habit at a Time

Motivation can be both helpful and misleading. When people decide to take control of their finances, they often try to change everything at once. They create a budget, start tracking expenses, set savings goals, research investing, commit to paying off debt, and promise themselves they’ll never overspend again. The enthusiasm is understandable.

The problem is that maintaining several major behavioural changes simultaneously is difficult.

This is one area where personal finance advice sometimes overlooks how habits are actually formed. Sustainable change tends to happen gradually. Trying to improve every aspect of your financial life at the same time can create unnecessary pressure and increase the likelihood of giving up altogether.

A more effective approach is to focus on a single improvement until it becomes part of your routine.

Perhaps that means reviewing your finances monthly. Perhaps it means automating savings. Perhaps it means reducing impulse purchases or creating a spending plan.

The specific habit matters less than your ability to maintain it consistently. Once that habit becomes established, you can build on it by introducing another positive change.

Think about personal finance the same way you would approach fitness. Most people would not expect to transform their health by following a perfect routine for two weeks. Progress comes from small actions repeated consistently over time. Managing money works in much the same way.

Strong money habits are rarely built through dramatic changes. They are usually the result of small decisions repeated often enough to become automatic.

7. Focus on Consistency Before Optimization

Many people spend a surprising amount of time searching for the perfect financial strategy.

They look for the ideal budgeting method, the best savings account, the most effective debt repayment plan, or the perfect investing approach. While these decisions matter, they are often less important than people assume.

A good plan that you follow consistently will almost always outperform a perfect plan that you abandon after a few weeks. This is one of the most overlooked lessons in personal finance.

People frequently delay action because they are waiting for certainty. They want to know they have chosen the best option before they begin. As a result, they spend months researching instead of taking meaningful action.

In reality, most financial success comes from consistency rather than optimization.

A simple spending plan followed for years is more valuable than an advanced budgeting system used for a month. Regular savings contributions matter more than endlessly comparing savings accounts. Consistent debt repayments typically produce better results than constantly switching strategies.

This doesn’t mean optimisation has no value. There will always be opportunities to improve your systems, refine your approach, and make better financial decisions. The key is understanding when optimization becomes a distraction.

A useful question to ask yourself is whether you’re improving your plan or avoiding execution. Sometimes the search for a better strategy is simply a more comfortable alternative to taking action.

The best money management tips are often the least exciting because they emphasize consistency over complexity. Yet those are the habits that tend to create lasting financial progress.

Consistency Beats Complexity

Most money management tips sound simple when you first hear them. Save more, spend less, avoid unnecessary debt, and plan ahead. The difficulty isn’t usually understanding the advice. It’s applying it consistently enough to see results.

That’s why the strongest financial habits are often the least impressive on the surface. They don’t rely on perfect budgeting, constant tracking, or finding the latest financial strategy. They rely on repeatable actions that fit naturally into everyday life.

If there’s one lesson worth taking from this guide, it’s that managing money successfully is rarely about doing everything at once. It’s about identifying a few behaviours that make sense for your situation and repeating them often enough that they become part of your routine.

Financial confidence isn’t built in a day. It’s built through small decisions that accumulate over time.

Start with one tip. Make it stick. Then build from there.

{kind=link}

No Comments