If you’ve spent any time researching budgeting methods, you’ve probably come across the term Zero-Based Budgeting (ZBB).

Table of Contents

- What Is Zero-Based Budgeting?

- How Zero-Based Budgeting Works

- What Happens If You Spend More in One Category?

- Why the Method Appeals to So Many People

- Why People Use Zero-Based Budgeting

- Advantages of Zero-Based Budgeting

- Potential Drawbacks of Zero-Based Budgeting

- Is Zero-Based Budgeting Better Than the 50/30/20 Rule?

- Who Should Use Zero-Based Budgeting?

- Final Thoughts

At first glance, the name can sound intimidating. It feels more like something an accountant, business owner, or government department would use than a practical budgeting method for everyday life. The phrase itself doesn’t offer many clues about how the system works, which is one reason many people overlook it.

In reality, zero-based budgeting is much simpler than it sounds.

The goal isn’t to track every dollar obsessively or create a budget so detailed that it becomes difficult to maintain. Instead, the purpose of zero-based budgeting is to give every dollar of income a purpose before it is spent. Rather than waiting until the end of the month to see where your money went, you decide in advance where your money should go.

This approach has made zero-based budgeting one of the most widely discussed budgeting methods in personal finance. Supporters appreciate the structure it provides, while critics argue that it can feel too restrictive or time-consuming. Like most financial systems, the truth lies somewhere in the middle.

For some people, zero-based budgeting creates clarity and control. For others, a simpler budgeting framework may be easier to maintain over time. Understanding the difference starts with understanding how the method actually works.

Before deciding whether zero-based budgeting is right for you, it’s worth exploring what the system is designed to do and why so many people continue to use it.

What Is Zero-Based Budgeting?

Zero-based budgeting is a budgeting method where every dollar of income is assigned a specific purpose before the month begins.

The objective is simple: income minus planned expenses should equal zero.

This doesn’t mean your bank account should reach zero. It means every dollar has been allocated somewhere within your budget.

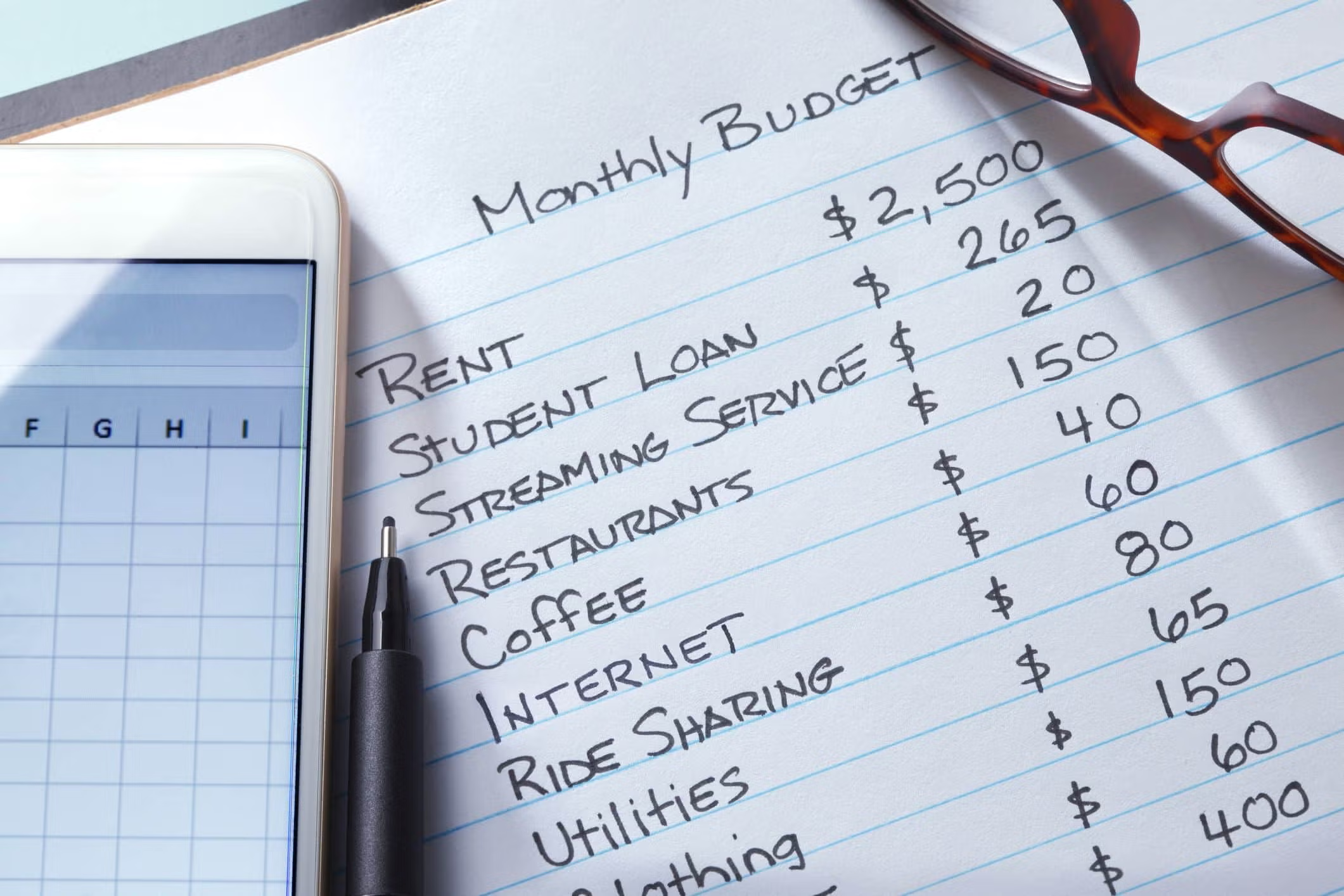

For example, imagine your monthly take-home income is $4,000.

Using a zero-based budgeting system, you might allocate:

- $1,500 to housing

- $400 to transportation

- $500 to groceries

- $300 to utilities

- $400 to savings

- $300 to debt repayment

- $300 to personal spending

- $300 to entertainment

Once all categories are assigned, the full $4,000 has a purpose.

At that point, your budget equals zero because there is no unassigned money remaining.

This is the foundation of the zero-based budgeting method.

Unlike some budgeting systems that focus primarily on spending limits, zero-based budgeting focuses on allocation. Every dollar is directed toward a specific goal, responsibility, or category before spending occurs.

This distinction is important because many people assume budgeting is about restricting spending. In reality, budgeting is primarily about making decisions. A budget helps determine where money should go rather than wondering where it went afterward.

One reason the zero-based budgeting definition often confuses people is the word “zero.” The term makes it sound as though the objective is to spend every dollar you earn. That isn’t the case.

Savings, investing, emergency funds, and debt repayment can all be assigned categories within a zero-based budget. Money that is intentionally allocated toward savings still has a job. It has simply been assigned to a future goal rather than a current expense.

This is why the zero-based budgeting meaning is often misunderstood. The system isn’t encouraging people to spend everything. It is encouraging people to plan for everything.

When viewed this way, zero-based budgeting becomes much easier to understand. The objective is not perfection. The objective is intentionality.

Of course, understanding the definition is only the first step. To see why so many people use zero-based budgeting, it’s helpful to look at exactly how the process works in practice.

How Zero-Based Budgeting Works

One reason zero-based budgeting has remained popular is that the process itself is relatively straightforward. While the name may sound complex, the method follows a simple sequence of steps that can be applied to almost any income level.

Every zero-based budget starts with income because you need to know how much money is available before deciding where it should go. For employees with a fixed salary, this calculation is usually straightforward. If your income varies from month to month, it’s often better to work with a conservative estimate based on previous earnings rather than income you hope to receive.

Once you know how much money is available, the next step is identifying your expenses and financial priorities.

These typically include:

- Housing

- Utilities

- Groceries

- Transportation

- Insurance

- Debt payments

- Savings contributions

- Personal spending

- Entertainment

- Other recurring expenses

The key difference with a zero-based budgeting system is that every category receives a planned amount before the month begins.

Let’s use a simple zero-based budgeting example. Imagine your monthly take-home income is $5,000.

You decide to allocate:

- $1,800 for housing

- $500 for groceries

- $350 for transportation

- $250 for utilities

- $400 for savings

- $300 for debt repayment

- $300 for entertainment

- $400 for personal spending

- $700 for other planned expenses

When the total reaches $5,000, your budget is complete. At this point, your income minus planned expenses equals zero.

Again, this doesn’t mean you have no money left. It means every dollar has already been assigned a purpose.

This planning process is what separates zero-based budgeting from many other budgeting methods. Rather than spending money throughout the month and reviewing the results afterward, you make spending decisions before money leaves your account. That shift alone can create greater awareness because every expense is considered within the context of a larger plan.

What Happens If You Spend More in One Category?

This is where many people assume zero-based budgeting becomes restrictive. In reality, a budget is not a contract.

Suppose you budgeted $500 for groceries but ended up spending $550. The solution isn’t to abandon the entire budget. Instead, you adjust another category to account for the difference.

Perhaps you spend $50 less on entertainment that month. Perhaps you reduce discretionary spending elsewhere.

The budget changes, but the overall plan remains intact.

This flexibility is important because life rarely unfolds exactly as expected. Unexpected expenses occur. Priorities change. Some categories require more attention than others.

Successful zero-based budgeting is not about predicting every expense perfectly. It is about creating a framework that helps you respond intentionally when circumstances change.

Why the Method Appeals to So Many People

Many budgeting systems focus primarily on controlling spending. Zero-based budgeting takes a slightly different approach.

Because every dollar is assigned in advance, people often feel more aware of where their money is going. This can make financial decisions feel more deliberate and reduce the uncertainty that comes from wondering whether there will be enough money left at the end of the month.

The method also encourages people to think about savings, debt repayment, and financial goals before discretionary spending takes place. Instead of saving whatever remains after spending, those priorities become part of the plan from the beginning.

For this reason, many people find that zero-based budgeting helps them become more intentional with money without necessarily requiring them to spend less.

The real appeal of the system isn’t that it creates perfect budgets. It’s that it creates visibility.

When every dollar has a purpose, it’s much easier to understand how your financial decisions align with your priorities.

Why People Use Zero-Based Budgeting

There is no shortage of budgeting methods available today. Some focus on broad spending categories. Others rely on percentage-based allocations. Some require detailed tracking, while others take a more hands-off approach.

Despite these options, zero-based budgeting continues to attract a loyal following.

One reason is that the method creates a strong sense of awareness. Because every dollar is assigned before the month begins, people often gain a clearer understanding of how their income is being used. Expenses that previously felt automatic become deliberate choices.

This visibility can be especially helpful for people who frequently find themselves wondering where their money went at the end of the month.

Zero-based budgeting also encourages intentional decision-making.

When money is allocated in advance, spending becomes less reactive. Rather than making financial decisions in the moment, you create a plan before competing priorities begin pulling your attention in different directions.

Another reason people use zero-based budgeting is that it naturally accommodates financial goals.

Whether you’re building an emergency fund, paying off debt, saving for a major purchase, or investing for the future, those goals become categories within the budget itself. They receive attention before discretionary spending occurs, making it easier to stay consistent over time.

Many people also appreciate the sense of control that the system provides.

Financial stress is not always caused by a lack of income. Sometimes it comes from uncertainty. When there is no clear plan for how money will be used, even a reasonable income can feel difficult to manage.

A zero-based budgeting method helps reduce some of that uncertainty by creating a roadmap for the month ahead.

Of course, no budgeting system is perfect. The same structure that some people find helpful may feel restrictive to others. To understand whether zero-based budgeting is the right fit, it’s important to look at both its strengths and its limitations.

Advantages of Zero-Based Budgeting

Every budgeting method has strengths and weaknesses, but there are several reasons why zero-based budgeting continues to be popular among people who want greater control over their finances.

One of the biggest advantages of zero-based budgeting is clarity. Because every dollar is assigned a purpose before the month begins, there is less uncertainty about where money should go. Essential expenses, savings goals, debt payments, and discretionary spending all have a place within the budget. This structure can make financial decisions feel less reactive because the most important priorities have already been considered in advance.

Another benefit of the zero-based budgeting method is that it encourages intentional spending. Many people don’t overspend because they lack discipline. They overspend because they make financial decisions without a clear plan. When income is allocated before spending occurs, it becomes easier to evaluate purchases against existing priorities. The budget provides a framework for decision-making rather than relying on willpower alone.

Zero-based budgeting can also be particularly effective for people working toward specific financial goals. Whether the objective is building an emergency fund, paying off debt, saving for a home, or increasing investments, the budgeting process requires those goals to be accounted for from the beginning. Instead of saving whatever remains at the end of the month, savings become part of the plan itself.

The system can also reveal spending patterns that might otherwise go unnoticed. When people create a zero-based budget for the first time, they often discover expenses that have become automatic over the years. Subscription services, recurring memberships, convenience purchases, and irregular spending habits become much more visible when every dollar needs to be assigned a category.

For some households, this increased awareness is one of the most valuable aspects of the zero-based budgeting system. The objective is not necessarily to reduce spending in every category. The objective is to understand how money is currently being used and determine whether that spending reflects personal priorities.

Another advantage of zero-based budgeting is flexibility. Although the method requires planning, it does not require perfection. Budget categories can be adjusted when circumstances change, and spending plans can evolve as new information becomes available. A budget is a tool designed to support decision-making, not a set of rules that must be followed without exception.

These advantages help explain why many people view zero-based budgeting as a practical way to manage money. At the same time, the features that make the system appealing to some people can create challenges for others.

Potential Drawbacks of Zero-Based Budgeting

While zero-based budgeting offers several benefits, it is not the ideal budgeting method for everyone. Understanding its limitations is just as important as understanding its advantages.

One of the most common criticisms of zero-based budgeting is the amount of planning involved. Because every dollar must be assigned a category, creating the budget typically requires more upfront effort than broader budgeting frameworks such as the 50/30/20 rule. For people who prefer simplicity or have little interest in regularly reviewing their finances, the process can feel unnecessarily detailed.

The method can also be more challenging for individuals with irregular income. When earnings vary significantly from month to month, assigning every dollar in advance becomes more complicated. Freelancers, contractors, business owners, and commission-based employees often need to revise their budgets frequently as income changes. While zero-based budgeting can still work in these situations, it usually requires additional flexibility.

Another potential drawback is the tendency toward perfectionism. Some people interpret zero-based budgeting as a requirement to predict every expense accurately and follow the budget exactly as written. When unexpected expenses occur or spending exceeds a category limit, they may view the budget as a failure rather than a tool that can be adjusted.

In practice, no budget will perfectly predict every financial decision. Life is unpredictable. Expenses arise unexpectedly, priorities change, and circumstances evolve throughout the month. The purpose of zero-based budgeting is not to eliminate uncertainty but to provide a framework for responding to it more intentionally.

There is also the risk of becoming overly focused on categorisation. A budget should support financial decision-making, not become a project that consumes excessive time and attention. If maintaining the budget requires more effort than the value it provides, the system may become difficult to sustain over the long term.

This is one reason personal finance often involves experimentation. A budgeting method that works exceptionally well for one person may feel restrictive or exhausting to another. The best budgeting system is rarely the most detailed or sophisticated. It is usually the one that a person can maintain consistently.

These limitations do not mean that zero-based budgeting is ineffective. They simply highlight an important reality: no budgeting framework works equally well for everyone. Choosing the right approach depends on your income, financial goals, personality, and willingness to engage with the budgeting process regularly.

Is Zero-Based Budgeting Better Than the 50/30/20 Rule?

Comparisons between budgeting methods often assume that one system must be better than the other. In reality, most budgeting frameworks are attempting to solve the same problem: helping people spend, save, and plan more intentionally.

The difference lies in how they approach that goal.

The 50/30/20 rule focuses on simplicity. Rather than assigning every dollar a specific purpose, it divides income into three broad categories: needs, wants, and savings. The framework provides structure while leaving plenty of flexibility within each category. For many people, this is enough. They don’t need to know exactly where every dollar is going. They simply need a system that keeps their finances moving in the right direction.

Zero-based budgeting takes a different approach. Instead of focusing on broad percentages, it asks you to decide where every dollar will go before the month begins. The result is often greater visibility and more control, but it also requires more planning.

This is why debates about budgeting methods can sometimes miss the point.

The real question is not whether zero-based budgeting is better than the 50/30/20 rule. The real question is how much structure you need.

Some people thrive with detailed plans. They want complete visibility into their spending and prefer making financial decisions in advance rather than adjusting throughout the month. For them, zero-based budgeting may feel natural.

Others prefer a simpler framework. They want guidance without having to manage numerous spending categories or make frequent budget adjustments. For these individuals, the 50/30/20 rule may feel more sustainable.

Both approaches can work.

The challenge is recognising that financial success rarely comes from finding the perfect budgeting method. More often, it comes from consistently using a budgeting method that fits your lifestyle, personality, and financial goals.

A budget that is slightly less detailed but used consistently will usually outperform a perfect budget that is abandoned after a few weeks.

Who Should Use Zero-Based Budgeting?

Zero-based budgeting is often recommended for people who want greater awareness of where their money is going.

If you’ve ever reached the end of the month wondering how your income disappeared despite having no major purchases to show for it, the structure provided by a zero-based budgeting system can be valuable. Assigning every dollar a purpose naturally increases awareness because spending decisions are considered before money leaves your account.

The method can also work well for people pursuing specific financial goals. Paying off debt, building an emergency fund, saving for a home, or increasing investment contributions often requires a deliberate plan. Zero-based budgeting helps ensure those priorities receive attention before discretionary spending takes place.

At the same time, it’s important not to assume that a more detailed budget automatically produces better results.

Many people maintain healthy finances without tracking every dollar. Others find that highly detailed budgeting systems create unnecessary friction and eventually become difficult to sustain. A budgeting method should support your financial life, not become an additional source of stress.

This is one reason personal finance advice can feel frustrating. People are often searching for the best budgeting system when the better question is whether a particular system fits the way they naturally make decisions.

Zero-based budgeting can be highly effective for someone who enjoys planning and wants greater control over their finances. For someone who prefers simplicity, a broader framework may produce better long-term results.

Neither approach is inherently superior. The goal is to find a system you can realistically maintain while continuing to make progress toward your financial goals.

Final Thoughts

Zero-based budgeting is often presented as a highly structured budgeting method, but its core principle is surprisingly simple. Rather than leaving spending decisions to chance, the system encourages you to decide where your money should go before the month begins.

For some people, that level of planning creates clarity and control. For others, a less detailed budgeting framework may feel more practical. Neither approach is inherently right or wrong because effective budgeting depends less on the method itself and more on whether the method can be maintained consistently.

If you’re considering zero-based budgeting, focus less on whether it’s the perfect system and more on whether it helps you become more intentional with your money. A budget does not need to be flawless to be effective. It simply needs to provide enough structure to support better financial decisions over time.

The best way to determine whether zero-based budgeting works for you is to try it. After all, no budgeting method can replace understanding how your own money is earned, spent, and managed.

{kind=link}

No Comments